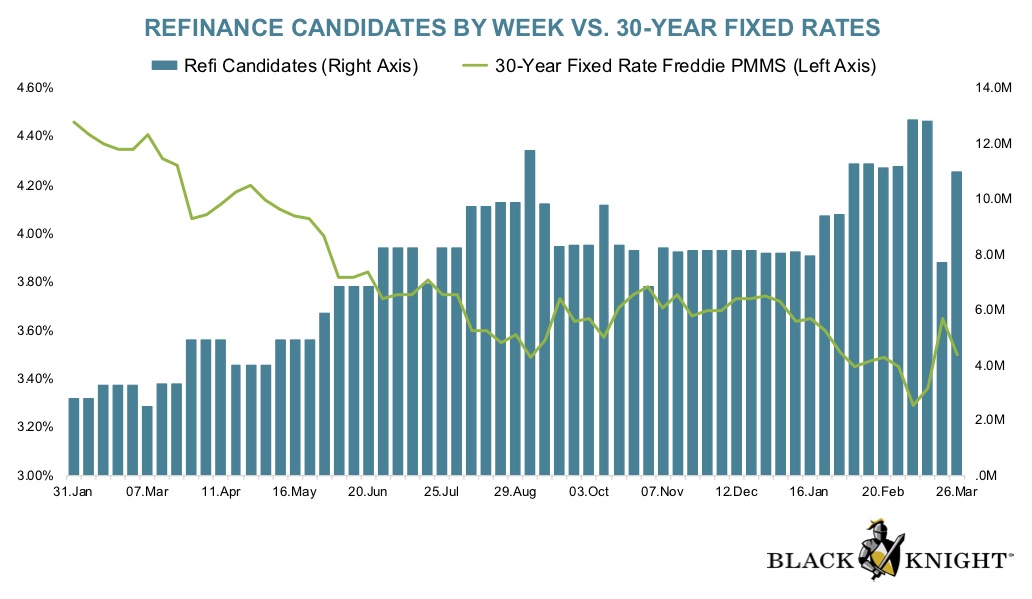

30-year mortgage rates averaged 3.36% the week of March 12.

At those near-record rates, data firm Black Knight estimated 13 million Americans could shave at least 0.75% off their rate by refinancing.

But rates are constantly in flux, which puts homeowners in a tough position.

Black Knight says rate changes as small as 0.125% could make the difference between refinancing or not for one million homeowners.

Not to mention, lenders are putting tougher standards in place that can make it harder to refinance in today’s market.

So — what’s a homeowner to do?

Verify your refinance eligibility at today’s rates (Apr 24th, 2020)

Is now a good time to refinance my mortgage?

Even in a coronavirus-driven economy, the basic rules for refinancing still apply. Shop around and make sure you’ll see worthwhile savings from any new loan.

As you shop for financing look for one or more of these benefits:

- Will your mortgage rate decline?

- Can refinancing result in lower monthly costs?

- Are monthly payment reductions sufficient to repay refinancing costs within 36 months?

- Can you switch from adjustable-rate financing to a fixed-rate and more certainty?

- Will you continue to own the property for enough time to recapture your refinancing costs?

If the answer to any of these questions is “yes,” a refinance would normally be worth considering.

But the question becomes more complicated in today’s environment.

With the mortgage industry in an unprecedented situation, borrowers are also facing new obstacles that can limit their ability to refinance. Your eligibility might be affected by:

- Higher credit score requirements

- Tighter loan-to-value maximums

- Unavailable loan types (jumbo loans, self-employed loans, government-backed loans, and more)

- A ban on rate locks until after approval

So while rates are low, some borrowers may not have access to the type of loan they need to make a refinance worthwhile.

Those least likely to be affected are “prime borrowers” — anyone with an excellent credit score, little debt, and a low loan-to-value ratio.

Consider your income stability

Refinancing is also more viable for those with plenty of job security, who aren’t put at direct financial risk by coronavirus.

Unless you qualify for a streamline refinance, your lender will need to verify your employment before you can refinance.

So you will likely be denied your refinance if you are about to be laid off or have already experienced a job loss or reduction in income.

The current coronavirus world is proving to be a tricky one for many members of society. There’s certainly no guarantee of refinancing success, even if you do decide it’s worth it.

Verify your new rate (Apr 24th, 2020)

But what if I refinance now, and rates drop again?

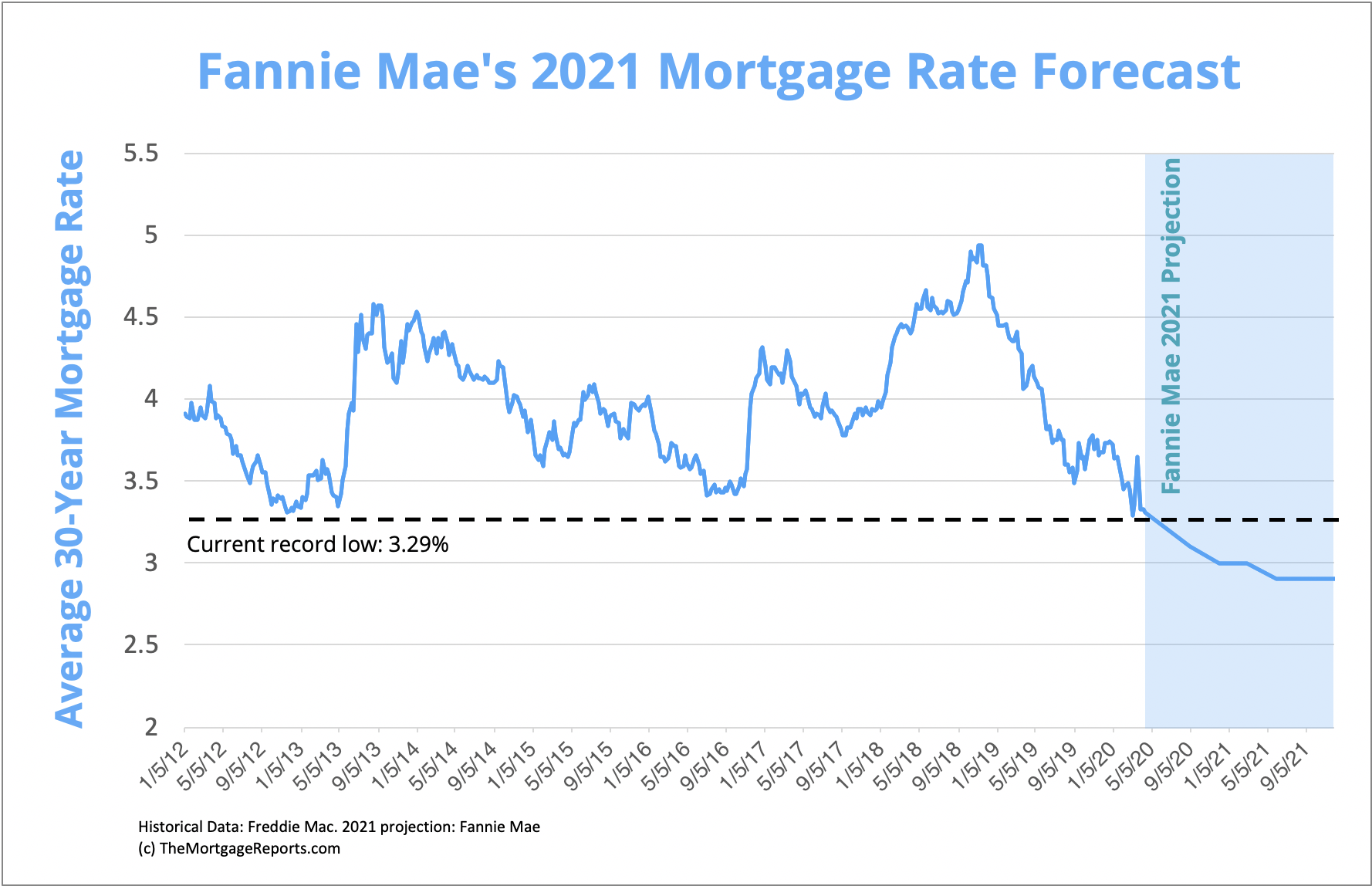

Mortgage rates have already fallen dramatically in 2019 and 2020. And some experts predict they’ll continue dropping — with rates averaging as low as 3% in 2020 and 2.9% in 2021.

See: Fannie Mae predicts 2.9% mortgage rates for 2021

In fact, there was speculation that mortgage rates would continue to fall in 2020 prior to the coronavirus.

Last June I wrote that “the very same factors which led to 3% financing are likely to lead us into the world of 2% mortgages. There’s an ongoing imbalance between investors with cash and people who want to borrow. Cash is everywhere and more of it is likely coming to a mortgage lender near you.”

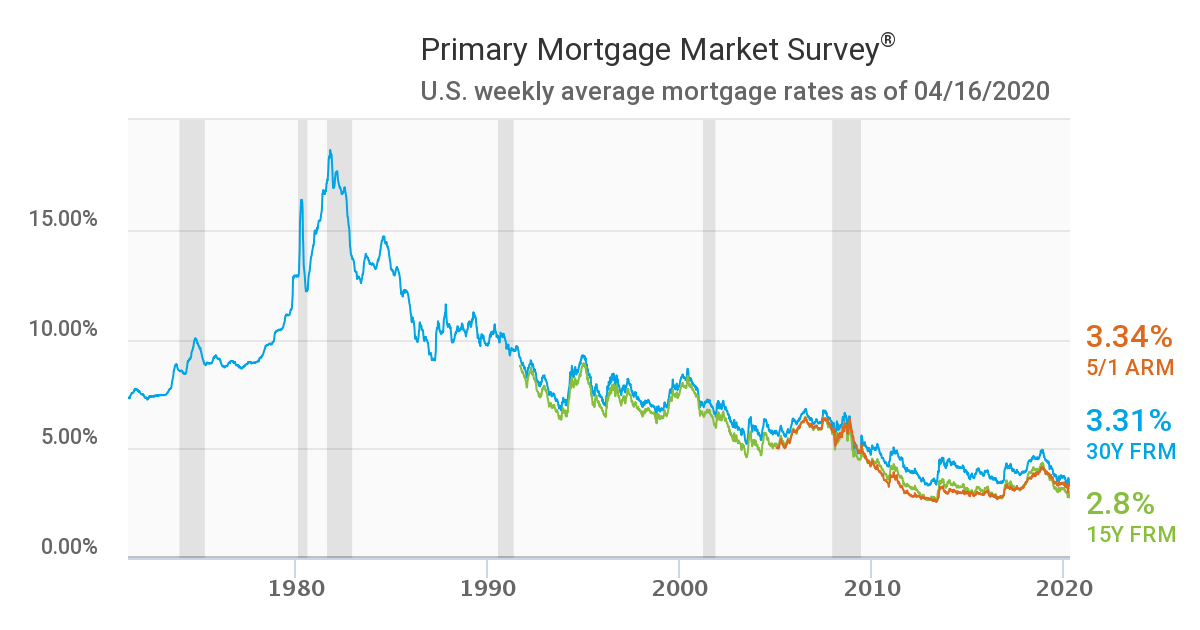

In fact, we now have 30-year rates in the 3.3% range and 15-year loans have crossed below the 3% barrier. In mid-April, 15-year mortgages were priced at 2.8% according to Freddie Mac.

Source: Freddie Mac Primary Mortgage Market Survey, week of April 16, 2020

But will those low-mortgage rate predictions really hold true in a post-COVID-19 economy?

The logic behind such predictions had to do with the supply and demand for capital.

We have had a massive cash surplus worldwide, paired with little demand. The result has been negative interest rates in both Asia and Europe and falling interest rates in the US.

Today we don’t know what we have. Will the world quickly get back to work? Or, are we in for months of shelter-in-place rules and closed workplaces?

All of these factors affect mortgage rates, which respond to the overall strength of the worldwide economy.

So although predictions say mortgage rates could continue falling, those predictions are never a guarantee.

Bottom line: If rates drop dramatically after a refinance, there’s always an opportunity to refinance again, opting for a no-closing-cost refi. This transaction involves taking a slightly higher-than-market rate — which could still be lower than your current rate — in exchange for the lender paying your closing costs.

Does a 0.125% rate change make refinancing worth it?

In its most recent report, Black Knight says “the population remains extremely sensitive to even the slightest rate movements, with a shift of 12.5 basis points (BPS) in either direction adding or subtracting more than a million borrowers from the potential refinance rolls.”

Translation: When rates rise as little as 0.125%, refinancing might go from ‘worth it’ to ‘not worth it’ for as many as one million homeowners.

When rates rise as little as 0.125%, refinancing might go from ‘worth it’ to ‘not worth it’ for as many as one million homeowners.

According to Black Knight’s definition, a homeowner is viable to refinance if they have: A credit score of 720 or higher, at least 20% equity in their home, and they can drop their rate by at least 0.75%.

That’s why the 0.125% rate change is important.

It’s not that you’d refinance to drop your rate by such a small amount. But rather, even small changes can shift the balance just enough to make a refinance worth it — or not.

Read more at The Mortgage Reports.

{Matzav.com}

{kind=link}